A tax tip for the business owners

If you’ve followed along the BEMag articles that have been in the money section for some time, you’d probably catch on that being efficient with tax is really important to me. Why? Because I love to work and I work hard and I want to keep the money I make so that it can be used more effectively to build the Kingdom. Amen?

So finding that I could learn everything I could about tax would benefit the end game of how much money was in my bank accounts, I started to run after it at a young age.

Over more than a decade of providing professional investment advice to wealthy Christian families and entrepreneurs, I learned a lot along the way through experience, from tax professionals and research. But most often, my experience comes from learning from people. Successful people.

On that note, haven’t we all seen the guy or girl on instagram recording some very catchy video on how to save tax but if their life was examined outside of social media, they wouldn’t have a leg to stand on? Don’t let me get started.

One of the best tax tips that I’ve seen save thousands and thousands of dollars for business owners is explained briefly in this article. A very recent consultation that I completed could save my client $20,000/year in taxes just from this one strategy with doing much differently.

“Hey, if I saw $20,000 on the floor, I’d pick it up!”

There’s a certain amount of money that business owners who are working within their business are taking out each year. Let’s call it - The draw. And The Draw is a set amount of how much that business owner needs to execute their regular personal expenses and is the rightful amount of pay they deserve for their work.

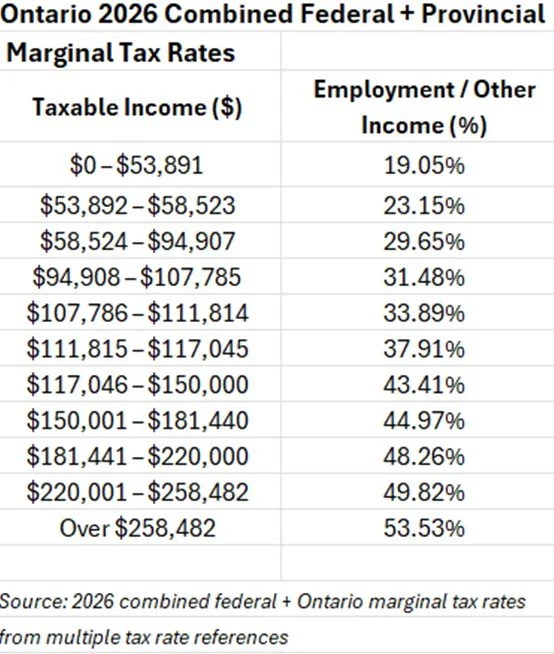

Many business owners and accountants classify The Draw as salary from the business to the owner. Salary, or employment income, tends to attract the highest tax rate that one could pay, given a few caveats in Canadian tax law. But the salary tends to be the go-to of accountants and payroll staff who are not as passionate about tax savings as many strategic tax pros could be. Let’s take a look at the taxes on employment income:

Salary or employment income in Ontario works on a marginal tax basis - the more dollars you make, the higher percentage of each additional dollar the government is going to request in taxes. And for business owners, The Draw that you’re taking, if it’s all salary, is being taxed according to these rates. The total tax is getting pretty crazy once you’re in the higher brackets as well.

The best low hanging fruit I see in tax consultations I have with my clients who work with me just for that purpose is in making The Draw more tax efficient so that these really high tax rates are not eating up all of their hard earned dollars.

This could accomplish two things:

1. Save money in the business by paying out less dollars to the owners because they owners will pay less tax

2. Equal amount of money leaves the corporation but the owners now have more left at the end of the day from the same draw.

How is this accomplished? By strategic assessment of the tax rate differential between how The Draw is being classified for taxes between salary or dividends or a mix of both.

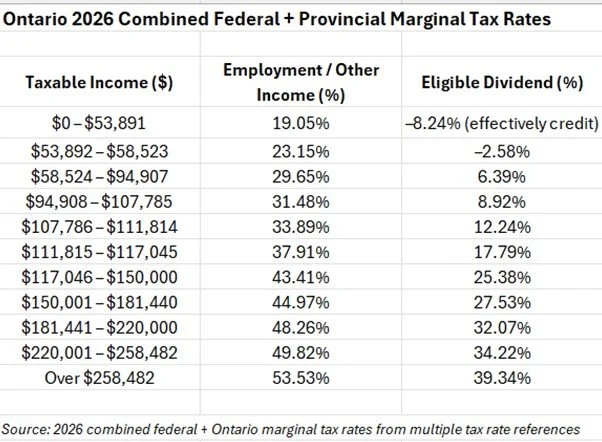

Here is a chart for Ontario residents combined marginal tax rates for 2026. Take a look at the difference in taxes between employment income and eligible dividends. And then tell me that you didn’t say… Holy Smokes! Because it’s huge.

Just reiterating the difference in the chart above, for business owners withdrawing in the range of $120,000/year, the tax on eligible dividends from your business vs salary is close to 1/3 of the tax. And for business owners withdrawing more, there’s still a huge savings of tax in the difference between the classification of the withdrawals.

This could be an opportunity that you’re leaving on the table for a variety of reasons. I’m just here to give you the lowest hanging fruit that I see on the tax strategy for my consulting clients.

One area that I’ve seen this backfire by leaning too hard in one direction or the other is in mortgage qualifications and lending. There are important things to consider, beyond just tax, when looking at your tax strategy. I wouldn’t want you to swap all of your income to dividends, save tax then not qualify for a mortgage on the house you want to buy next year because your lender is looking for employment income on your tax returns.

Another area is in the final calculations not being followed thru with this strategy so the accountants don’t have the correct or updated information to reflect this strategy when the year end processing is being worked on.

As many nuances as there are in taxes and thinking big picture, I’d want you to know that this option is something to explore.

Ask me anything - I love saving tax for me, and for you.